When firearms manufacturing equipment breaks down, the financial impact can be severe: halted production, costly repairs, and potential contract breaches. Standard property insurance often excludes mechanical failures, leaving manufacturers exposed. To address this, specialized policies like Equipment Breakdown Insurance, Commercial Property Insurance, and Inland Marine Insurance are critical. These cover internal failures, external threats (e.g., fire, theft), and equipment in transit, respectively.

For firearms manufacturers, combining these policies with Workers' Compensation and General Liability Insurance provides a solid risk management plan. This approach ensures protection for machinery, employees, and third-party claims, helping businesses maintain operations and meet compliance standards.

Joseph Chiarello & Co., Inc., with over 40 years of experience, offers tailored insurance solutions for the firearms industry, including admitted policies backed by state insurance departments. Their services also include claims handling, loss control, and underwriting support to minimize downtime and financial losses.

Firearms manufacturers face challenges that can disrupt production and strain finances. Recognizing these risks is crucial for safeguarding operations against unexpected setbacks.

Electrical issues often lead to equipment breakdowns. Power surges from lightning strikes or faulty wiring can instantly damage sensitive components, while smaller, repeated surges gradually wear down machinery over time [3].

Automation plays a central role in modern firearms manufacturing, with computer programming managing entire processes. Eddie Dreyer, Commercial Lines Staff Underwriter at Central Insurance, highlights this vulnerability:

"So much of manufacturing is automated, where computer programming runs the process. That's still equipment, and it's still exposed to failures" [4].

Failures can also stem from lack of proper maintenance and operator mistakes. Skipping routine upkeep or disregarding manufacturer guidelines often leads to preventable breakdowns [3][4]. The situation worsens when outdated parts are involved, as sourcing replacements can take time and extend downtime [4].

External factors add another layer of risk to manufacturing equipment.

Fire damage can impact more than just the areas touched by flames. Smoke and water from firefighting efforts can harm machinery and inventory. Doug Larson, an insurance expert, emphasizes this hidden danger:

"Smoke and water are deceptively destructive, so even if the flames don't touch some parts of the building or your inventory, repairs or cleanup will probably be needed" [5].

Theft of high-value equipment not only causes immediate financial loss but can also lead to regulatory issues, particularly if inventory goes missing [5]. Meanwhile, natural disasters like flooding or extreme humidity can severely damage critical components and electrical systems [3][4].

Specialized machinery used in firearms manufacturing faces distinct challenges. Precision tools, such as barrel rifling machines and automated assembly systems, are often difficult to replace. These machines aren’t typically available from local suppliers, which can lead to extended production delays. Dreyer underscores the importance of quick repairs:

"If a machine goes down, can they get parts in a couple of days, or will it take six months? The quicker they can repair or replace, the less of a true business income loss they face" [4].

Compliance requirements further complicate matters. Equipment must meet OSHA standards for lead and noise exposure, as well as ATF marking regulations [6]. A breakdown could result in compliance violations, jeopardizing contracts with military or law enforcement agencies [4]. Considering that the value of U.S. manufacturing equipment reached about $1.8 trillion in 2022 [4], even one specialized machine failure can lead to significant financial consequences.

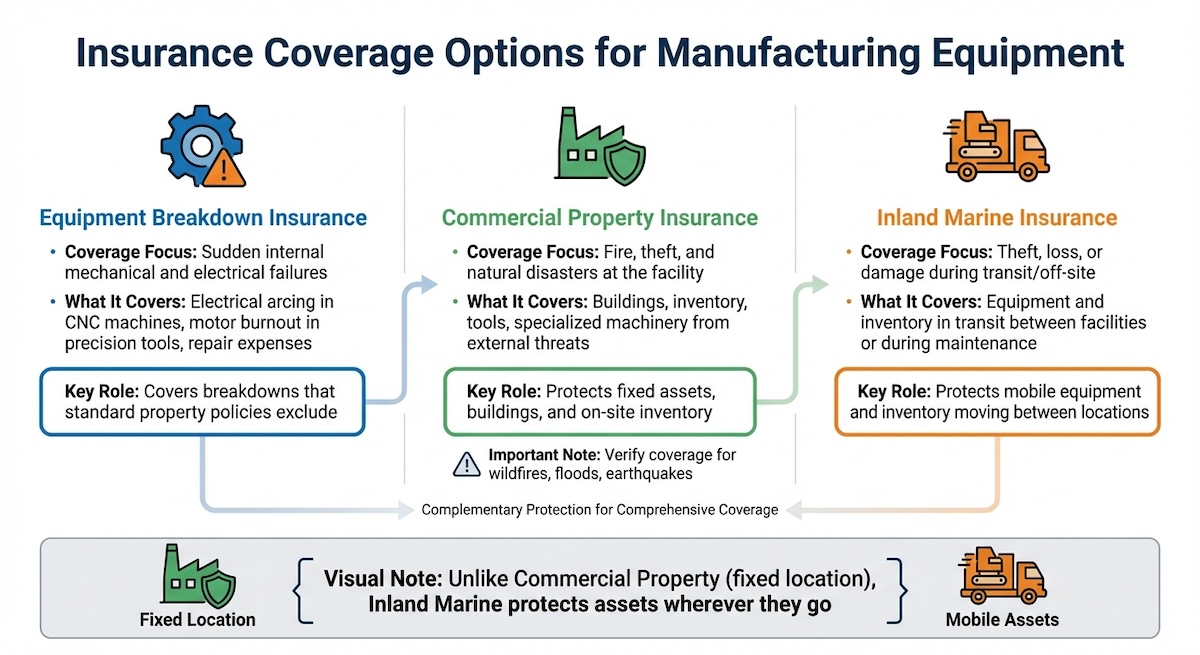

When it comes to manufacturing, standard insurance policies often leave gaps that could expose businesses to unexpected costs. To address these vulnerabilities, there are specialized coverage options designed to protect against specific risks tied to manufacturing equipment.

Equipment Breakdown Insurance steps in when internal mechanical or electrical failures occur - issues that typical property insurance won’t cover. Think of situations like electrical arcing in a CNC machine or a motor burnout in precision tools. This type of coverage helps cover repair expenses, ensuring that downtime is kept to a minimum and operations can resume quickly[7].

Commercial Property Insurance focuses on safeguarding physical assets such as buildings, inventory, tools, and specialized machinery from external threats like fire, theft, or natural disasters[10][11]. However, it’s essential for manufacturers to confirm whether specific risks like wildfires, floods, or earthquakes are explicitly included in their policy[9][8]. Without these inclusions, recovery after a natural disaster could result in significant out-of-pocket costs.

Inland Marine Insurance provides protection for equipment and inventory while they’re in transit or stored off-site. This is especially critical for manufacturers who frequently move specialized equipment between facilities or send it out for maintenance. As Joseph Chiarello & Co., Inc. explains:

"Insurance can offer coverage for such losses... whether your firearms are lost in transit, misplaced, or damaged beyond repair"[12].

Unlike Commercial Property Insurance, which covers assets at a fixed location[11], Inland Marine Insurance ensures mobile assets are protected wherever they go[12].

For over four decades, Joseph Chiarello & Co., Inc. has specialized in Firearms Business and Property Insurance, addressing the unique risks faced by manufacturers. This coverage is designed to protect industrial equipment, machinery, and fixtures from disasters like fires, floods, and other natural events[10][13]. A key feature of this policy is Equipment Breakdown Insurance (also known as Boiler and Machinery coverage), which handles sudden mechanical failures. This includes covering the costs of repairs and compensating for potential income losses caused by these breakdowns[1][2].

The company offers admitted policies, which are backed by the state insurance department where they’re issued. This ensures a level of long-term security and reliability for manufacturers[8][14]. Whether you're a small accessory maker or a large-scale manufacturer, this coverage is tailored to fit businesses of all sizes[10]. As one client, Fritz S., put it:

"A first-class broker representing the insured."[10]

To complement their robust coverage, Joseph Chiarello & Co., Inc. also provides extensive support services aimed at reducing downtime and managing risks effectively.

In addition to primary insurance policies, the company offers specialized services to further protect its clients' operations. Their Loss Control Insurance helps manufacturers identify and address operational risks before they escalate into equipment failures or property damage[13][14].

The firm’s Insurance Claims Handling team plays a hands-on role in managing claims. They work directly with appraisers and contractors to assess damages promptly, ensuring a faster recovery and a quicker return to normal business operations[15].

The Insurance Underwriting services take a close look at factors like equipment type and age, helping to determine the right coverage while offering proactive recommendations to reduce risks[16]. Additionally, Employee Background Checks are available to help manufacturers vet new hires, reducing the chances of theft or negligence within their operations[13]. Client Charles K. praised their approach, saying:

"Their service has been outstanding. I would strongly recommend them to any gun dealer in need of insurance for their business."[10]

Relying solely on machinery coverage isn't enough to shield firearms manufacturers from the wide range of risks they face. A well-rounded strategy blends multiple insurance policies to cover overlapping vulnerabilities effectively.

Firearms manufacturing is inherently high-risk, where equipment breakdowns and workplace injuries can occur simultaneously. Imagine a scenario where a defective press not only damages machinery but also injures a worker. In such a case, equipment breakdown insurance might cover $50,000 in repairs, while Workers' Compensation takes care of $20,000 in medical expenses and lost wages. Without these policies, your business could face hefty out-of-pocket costs, plus potential production halts that might result in daily revenue losses exceeding $100,000. Together, these policies help manage repair and medical expenses while ensuring your operations stay on track.

Workers' Compensation insurance is a legal requirement in most U.S. states, designed to address employee injuries. It complements machinery coverage by also covering compliance-related expenses, such as mandatory safety training or OSHA fines tied to equipment failures. For example, if faulty machinery leads to an injury, Workers' Compensation handles the injury claim, while machinery insurance can fund necessary upgrades to meet ATF and OSHA standards. This could help avoid penalties that can reach $15,000 per violation. By combining these policies, you protect both your employees and your production capabilities when mechanical issues arise.

While Workers' Compensation focuses on internal risks, Commercial General Liability (CGL) Insurance addresses external liabilities. CGL protects against third-party claims, such as injuries or property damage caused by defective products. For instance, if a malfunctioning machine produces faulty firearm parts that injure a distributor or damage their facility, CGL can cover legal defense costs, settlements, and medical expenses. Coverage limits typically start at $1 million per occurrence, and many small businesses opt for policies with $1 million per occurrence and $2 million in aggregate for sufficient protection.

Consider a situation where defective barrels from a machine malfunction injure a retailer during testing. In this case, machinery coverage might pay $75,000 for equipment repairs, Workers' Compensation would cover internal injuries, and CGL would handle the $500,000 third-party claim, including legal fees. For a mid-sized firearms manufacturer with 50 employees and $5 million in revenue, bundling these policies - machinery coverage (around $10,000–$20,000 annually), Workers' Compensation (approximately $50,000–$100,000), and CGL (roughly $15,000–$30,000) - through an insurance specialist can result in multi-policy discounts of 10–20%.

This combination of coverage forms a robust risk management strategy, ensuring firearms manufacturers are prepared for a variety of challenges. Joseph Chiarello & Co., Inc. specializes in providing integrated insurance solutions for comprehensive protection across the U.S.

Manufacturing firearms requires precision equipment and uninterrupted operations to stay competitive in a demanding industry. When critical machinery breaks down, the ripple effects can be devastating - repair costs, production halts, missed deadlines, and lost revenue. Standard property insurance often falls short here, leaving businesses exposed. That’s where machinery-specific insurance steps in, covering internal breakdowns and offering a safety net tailored to the industry's unique needs.

Joseph Chiarello & Co., Inc. brings over 40 years of experience to the table, specializing in underwriting and loss control solutions designed for the firearms industry. As the endorsed insurance provider for the National Shooting Sports Foundation (NSSF), they understand the challenges of protecting high-value machinery and specialized inventory. Their admitted policies, backed by state insurance departments, offer manufacturers financial security and peace of mind when it matters most.

"A first class Insurance Broker representing the insured not the insurance company. They are the very best in the business!" - Fritz S.

An effective risk management strategy goes beyond machinery coverage. Pairing it with Workers' Compensation and Commercial General Liability Insurance creates a comprehensive safety net. This approach not only protects equipment and employees but also addresses third-party claims and compliance requirements. Joseph Chiarello & Co., Inc. helps manufacturers streamline risk management by bundling these policies, reducing coverage gaps, and delivering cost savings.

Having a trusted insurance partner means you can focus on production instead of worrying about unexpected setbacks. By working with experts who understand the complexities of firearms manufacturing - like equipment specifics, facility locations, and operational scales - you can secure the right coverage to protect your operations and support long-term growth. A well-planned insurance strategy ensures business continuity and allows manufacturers to move forward with confidence.

A "breakdown" claim involves the sudden and accidental failure of equipment or machinery caused by an unforeseen event. This type of claim doesn’t apply to damage resulting from wear and tear, lack of proper maintenance, or neglect. Instead, it typically covers unexpected mechanical or electrical malfunctions that interrupt operations.

If you don’t often transport machinery, Inland Marine insurance might not be necessary. This type of coverage is designed for property that’s regularly on the move. However, if your equipment is valuable and occasionally relocated or stored in various places, it could still offer important protection. Assess your situation carefully to decide if this coverage aligns with your needs.

When deciding on coverage limits for specialized machinery in firearms manufacturing, it's crucial to weigh the risks and financial consequences of potential claims or damages. Start by assessing the value and role of each machine - factor in repair or replacement costs and any liability they might create. To make sure your coverage fits your needs, work with an insurance specialist who understands the unique challenges of firearms manufacturing. This way, you can protect your equipment effectively and avoid the pitfalls of underinsurance or unexpected costs.

Don't wait until it's too late to make sure your gun shop is covered. At Joseph Chiarello & Co., Inc., we’re here to help you navigate the ins and outs of gun shop workers compensation insurance to ensure you're prepared for any noise-related risks, including hearing damage. Reach out to us today to review your current policy or get a customized quote. Protect your team and your business with the right coverage—because their safety is worth it.

Call Now: 800-526-2199. Or submit your inquiry below. We look forward to having the opportunity to work with you!