When evaluating the insurance options provided by Joseph Chiarello & Co., Inc., firearms retailers need to weigh the benefits and limitations of each policy to create a well-rounded coverage plan.

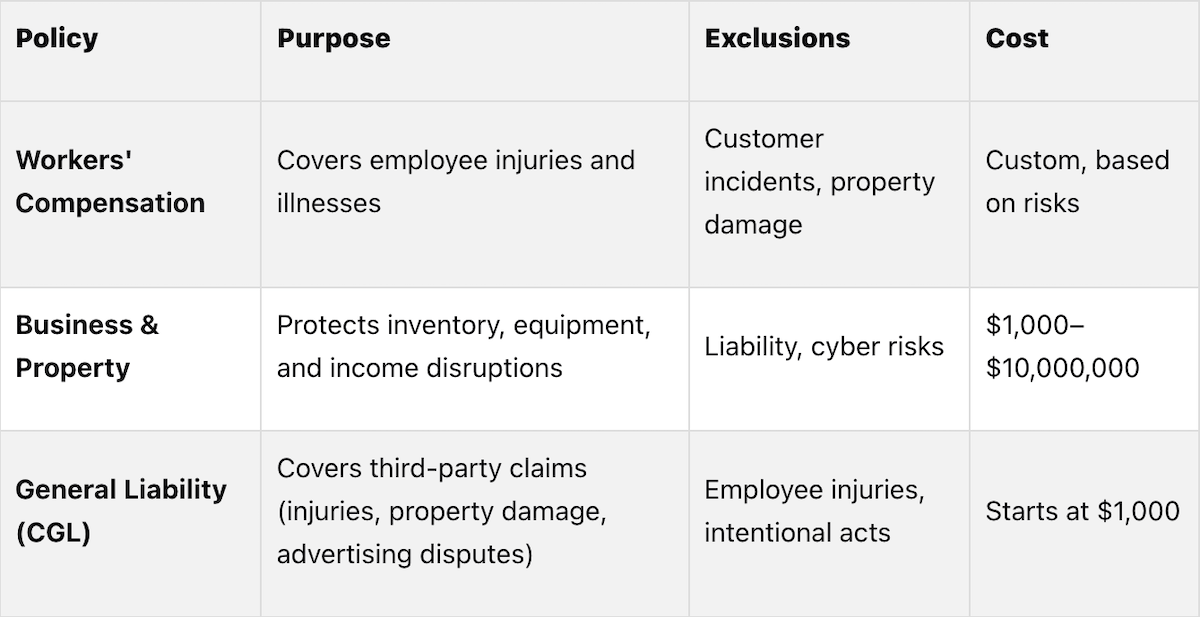

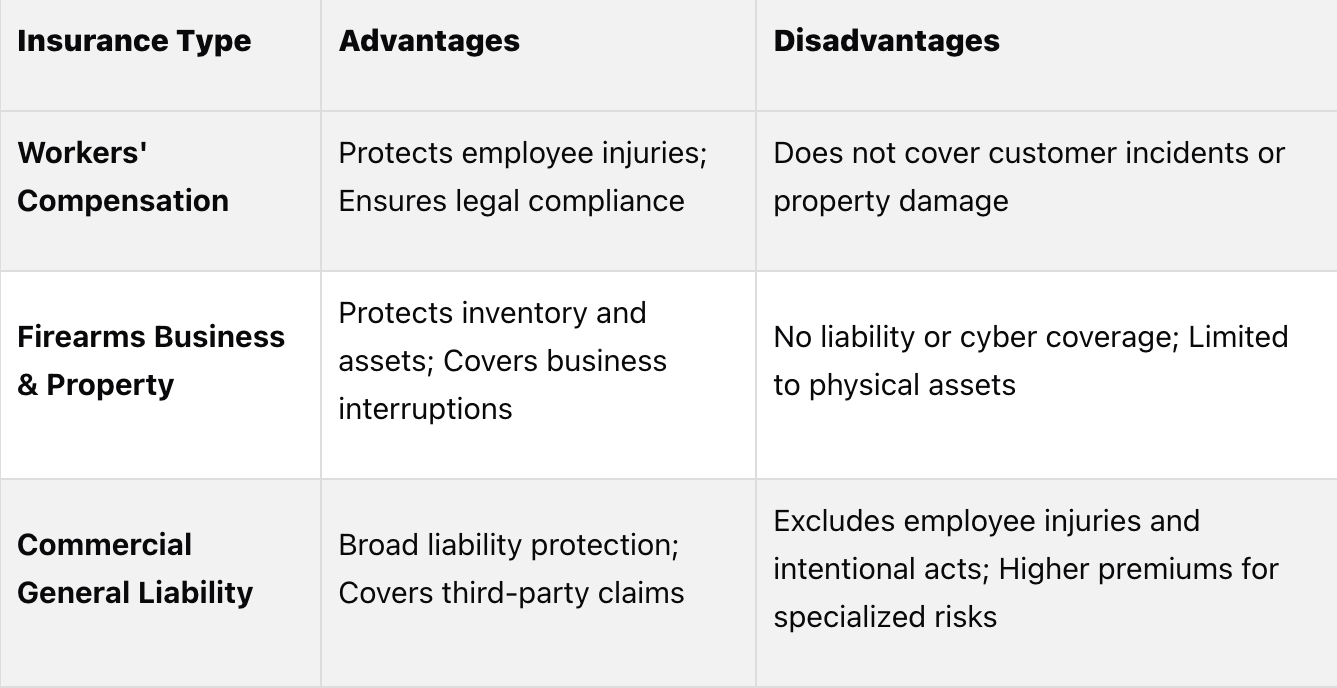

Workers' Compensation Insurance is a must-have for protecting employees from workplace injuries, especially in environments where handling firearms and ammunition poses unique risks. This coverage ensures compliance with state laws and promotes a safer work environment. However, its scope is limited - it only covers employee injuries and excludes incidents involving customers or property damage.

Firearms Business and Property Insurance is designed to protect physical assets, inventory, and business operations from disruptions like fire, theft, or other industry-specific risks. For firearms retailers, this is critical given the high value of their inventory and specialized equipment. On the downside, this policy does not include liability or cyber protection, focusing exclusively on physical assets.

Commercial General Liability Insurance provides the broadest coverage, addressing third-party claims, legal defense costs, and liability scenarios. It's a popular choice among small business owners, with 91% of Insureon customers selecting coverage limits of $1 million per occurrence and $2 million aggregate [14]. This policy covers bodily injury, property damage, and advertising-related claims, but it excludes employee injuries and intentional acts, and premiums can be higher due to the specialized risks involved [15].

Gun shops face strict regulations, higher liability risks, and potential lawsuits. Many insurers lack expertise in this niche, making specialized policies crucial for compliance and financial security. Combining these policies ensures well-rounded protection for your employees, assets, and legal liabilities.

A layered insurance approach is the best way to safeguard firearms retailers from financial, legal, and operational risks.

With over 40 years of experience and the endorsement of the National Shooting Sports Foundation, Joseph Chiarello & Co., Inc. offers Workers' Compensation Insurance specifically designed for firearms retailers [2]. This specialized coverage protects both employees and businesses from the financial impact of work-related injuries or illnesses, addressing the unique risks associated with the firearms retail industry [2].

Interestingly, gunshot-related injuries are not the primary source of workers' claims in this field. Instead, claims typically stem from issues like noise-induced hearing loss, lead exposure from handling ammunition, injuries from manual lifting, and minor cuts or bruises sustained during daily operations [4]. The policy covers essential costs such as medical expenses, disability benefits, and rehabilitation for injured employees [3].

These benefits, paired with tailored premium models, provide comprehensive protection that aligns with each business's specific risk profile.

Customer testimonials highlight the reliability of this service. Charles K. shared, "Their service has been outstanding. I would strongly recommend them to any gun dealer in need of insurance for their business" [2][3]. Similarly, Brian K. stated, "The staff has been great over the years we have been customers of theirs. They have always responded extremely quickly" [2][3].

The cost of Workers' Compensation Insurance is determined using a custom pricing model based on factors like business size, employee count, operational details, and overall risk exposure. Non-compliance with workers' compensation requirements can lead to severe penalties, including hefty fines, legal actions, and even license suspension [3].

This type of specialized coverage is critical, as many insurance providers lack the expertise to properly assess the risks associated with firearm-related businesses. As a result, they often decline coverage rather than invest the time to understand this niche industry [4].

Joseph Chiarello & Co., Inc. provides specialized commercial property insurance designed to protect firearms retailers from disasters, theft, and crime [5]. This type of coverage, combined with Workers' Compensation, is a key part of a firearms retailer’s risk management plan. It addresses standard business risks while also considering the unique challenges faced by gun stores, such as higher exposure to theft, burglary, and other security concerns [5]. Given the vulnerability of firearms retailers to natural disasters and criminal activities, property insurance is crucial for maintaining business operations and ensuring peace of mind [5]. Let’s break down the specific coverages that safeguard your property and business.

The Firearms Business and Property Insurance policy is tailored to the risks firearms retailers encounter. For instance:

Additional coverage includes boiler and machinery protection, glass and sign coverage for storefront damage, and protection for valuable papers and records. The policy also addresses equipment breakdown and accidental inventory loss [5][6]. Optional flood and earthquake coverage is available, though eligibility may vary based on location [5]. Liability claims for accidental injuries or property damage caused by firearms are also covered [6].

This insurance offers broad financial protection tailored specifically to the firearms retail industry. By bundling coverage for multiple risks into one policy, it simplifies insurance management. A standout feature is its admitted policy status, meaning the coverage is backed by the state insurance department where it’s issued, adding a layer of regulatory protection [9].

Customizable limits allow businesses to adjust property and replacement cost coverage based on their specific risks. Additionally, the endorsement from the National Shooting Sports Foundation underscores the policy’s reliability and suitability for firearms retailers [10][11].

The policy does not cover losses resulting from intentional or criminal acts, nor harm that exceeds reasonable self-defense [7][8]. Employee injuries fall under Workers' Compensation rather than property insurance [8]. Other exclusions include damage caused by poor maintenance, preventable third-party claims, and subcontractor-related issues, which would require separate coverage [8].

The pricing is structured to accommodate businesses of all sizes, with premiums ranging from $1,000 to $10,000,000 [10]. This flexibility ensures that both small and large firearms retailers can find coverage that fits their needs. SAFTEA instructors can access specialized pricing starting at $375, though additional fees may apply in states like New Jersey, Florida, and Kentucky [11].

Premiums are determined by factors such as business size, inventory value, location risk, and operational specifics. Property limits and replacement costs can be customized to match the actual risk exposure and asset value of the business [11]. The admitted policy structure ensures regulatory protection, providing confidence that the coverage aligns with your overall risk management strategy [9].

Joseph Chiarello & Co., Inc. offers a Commercial General Liability (CGL) insurance policy tailored specifically for firearms retailers. This policy is designed to address liability concerns like property damage, personal injury, or advertising-related claims that may arise from business operations [12]. With over 40 years of experience in the firearms industry [10], the company has developed solutions that align with the unique challenges faced by gun shops.

The CGL policy provides coverage for both legal defense costs and damages, up to the policy limits [12]. This dual approach helps protect firearms retailers from the financial strain of lawsuits, including settlement or judgment expenses. Additional features include risk assessments, customized coverage options, regulatory compliance guidance, claims assistance, and policy reviews [1].

Bodily Injury and Property Damage Liability

This coverage applies to legal liabilities for bodily injuries or property damage caused by the business's premises, operations, or non-professional negligence [12]. It also extends to mental and emotional distress categorized as bodily injuries [12].

Personal and Advertising Injury

This protection covers claims such as libel, slander, copyright infringement, false arrest, malicious prosecution, wrongful eviction, invasion of privacy, and misuse of advertising ideas [12]. For firearms retailers involved in advertising or social media, this coverage is especially relevant.

Medical Payments

This feature provides limited coverage for injuries suffered by non-employees due to accidents on the business premises or during operations. Importantly, it does not require legal action to trigger the coverage [12]. Together, these elements create a robust financial safety net for firearms businesses.

The CGL insurance policy offers firearms retailers protection against lawsuits and claims by covering both legal defense costs and damages [12]. This ensures businesses can navigate litigation without facing overwhelming financial pressures.

Additionally, the policy helps businesses stay compliant with the complex regulations governing the firearms industry [1]. Joseph Chiarello & Co., Inc. provides tailored insurance solutions and dedicated claims support to meet the specific needs of each retailer [1].

Certain areas are excluded from the base policy, such as workers' compensation and employment practices liability insurance, which must be purchased separately [12]. This means injuries to employees or employment-related disputes require additional coverage. Pollution liability is also excluded but can be added through endorsements or separate policies [12].

Other exclusions include liquor liability, professional liability, auto liability, and risks tied to intentional acts or criminal behavior. These exclusions align with standard industry practices [13].

The pricing for Joseph Chiarello & Co., Inc.'s CGL insurance is structured to be accessible for firearms retailers of various sizes, with a minimum premium starting at $1,000 [10]. The base policy includes a $1,000,000 per occurrence limit and a $2,000,000 aggregate limit [9]. For businesses with greater exposure, higher limits are available, allowing retailers to adjust their coverage based on factors like location, size, and operational risks [9].

A layered insurance strategy is necessary to address these gaps. For instance, Workers' Compensation doesn’t cover customer-related incidents, Firearms Business and Property Insurance lacks liability protection, and Commercial General Liability excludes employee injuries and intentional actions [15]. Combining these policies ensures more comprehensive protection.

On average, General Liability Insurance costs $42 per month (around $500 annually) [14], but specialized policies often come with higher premiums due to increased risks [16]. For smaller retailers, the cumulative cost of multiple policies can be a challenge, potentially leaving them underinsured.

Beyond financial protection, comprehensive insurance also enhances risk management by helping retailers identify and prepare for potential hazards [15]. Over time, this proactive approach can lead to better safety measures and fewer incidents.

Finally, these policies help retailers meet various legal and regulatory requirements, from workplace safety to liability standards, reducing administrative burdens while ensuring compliance with industry rules. However, smaller businesses may struggle with scalability, as the cost of securing all-encompassing coverage can be prohibitive.

Ultimately, a layered coverage approach is essential for addressing the unique risks faced by firearms retailers, ensuring they remain protected while navigating the complexities of their industry.

Choosing the right insurance coverage for your firearms retail business involves finding the right balance between thorough protection and practical business needs. Joseph Chiarello & Co., Inc. offers three key policies, each addressing specific risks and helping build a well-rounded insurance plan.

Workers' Compensation Insurance is a cornerstone for protecting employees and ensuring legal compliance. This policy is critical for meeting state requirements while safeguarding workers against job-related injuries.

Firearms Business and Property Insurance focuses on securing your inventory, equipment, and physical location from risks like theft, fire, and natural disasters. However, it’s important to note that this policy does not include liability coverage.

Commercial General Liability Insurance provides essential protection against third-party claims, addressing the inherent liability risks that come with operating a firearms retail business.

Together, these policies create a comprehensive safety net. As Daniels-Head Insurance Agency puts it, "Insurance, for anything, is the transfer of risk and an investment in financial security" [18]. This perspective emphasizes the importance of viewing insurance as a proactive risk management tool rather than just an expense.

When assessing your insurance needs, consider factors such as the size of your business, the value of your inventory, specific risks tied to your location, and applicable regulatory requirements. Underwriting services for firearms retailers take into account factors like your location, security measures, and claims history [17].

Working with specialists at Joseph Chiarello & Co., Inc. ensures your coverage is tailored to the unique challenges and compliance requirements of the firearms retail industry. Their expertise can help align your policies with the specific risks your business faces.

If your risk exposure increases, consider raising your coverage limits [18] to protect against potentially significant financial losses. Additionally, make it a habit to review and update your insurance regularly. Changes in inventory, business practices, or regulations may require adjustments to your policies, ensuring your coverage evolves alongside your business.

The firearms retail industry comes with distinct challenges, but with the right combination of Workers' Compensation, Firearms Business and Property, and Commercial General Liability insurance, you can secure robust protection against a wide range of risks while staying compliant with industry regulations.

Firearms retailers operate in a high-risk environment that demands specialized insurance coverage. Key concerns include theft, property damage, and product liability claims resulting from firearm malfunctions or misuse. On top of that, these businesses must adhere to strict regulatory requirements, where even minor missteps can lead to hefty legal or financial penalties.

Other pressing risks involve cybersecurity threats targeting sensitive customer and transaction data, employee safety issues, and liabilities tied to accidents involving firearms. Tailored insurance coverage is essential to address these challenges, providing protection that aligns with the specific needs of the firearms industry.

Workers' Compensation Insurance for firearms retailers is crafted to address the distinct challenges of the industry, including the handling of firearms and ammunition, as well as maintaining safety in a higher-risk work environment. While standard workers' compensation policies cover common workplace injuries, they often fall short when it comes to the specialized risks that firearms businesses encounter.

Tailored policies provide firearms retailers with coverage that aligns with their specific operations. This ensures they not only comply with safety regulations but also manage the unique risks associated with their industry effectively.

A layered insurance strategy is crucial for firearms retailers because it addresses the specific challenges and risks that come with the industry. These risks include product liability, property damage, and cybersecurity threats. By adopting this approach, businesses can minimize financial vulnerabilities and stay resilient in the face of unexpected incidents without disrupting their operations.

Operating without sufficient insurance leaves firearms retailers exposed to significant financial strains, such as expensive legal battles, settlements, and interruptions to business activities. These gaps in coverage can result in serious repercussions, including loss of revenue, harm to the company's reputation, and, in some cases, the risk of shutting down entirely. With tailored, multi-layered insurance in place, firearms retailers can better protect their businesses and maintain stability in an industry that is both highly regulated and fraught with risks.

There are different policy options available for gun shop owners. Consulting with specialists is crucial to fully analyze and identify the proper policy that your business needs. Seek out experts who have had years of experience handling insurance coverage specifically for firearms distributors and stores.

Joseph Chiarello & Co., Inc has provided gun store owners throughout the United States with crucial advice and guidance in getting the appropriate insurance policies for their property and their business. These policies protect your business and defend your rights as firearm retailers.

Consult with our specialists to protect your property today. You may also browse our resources to learn more.

Call Now: 800-526-2199. Or submit your inquiry below. We look forward to having the opportunity to work with you!