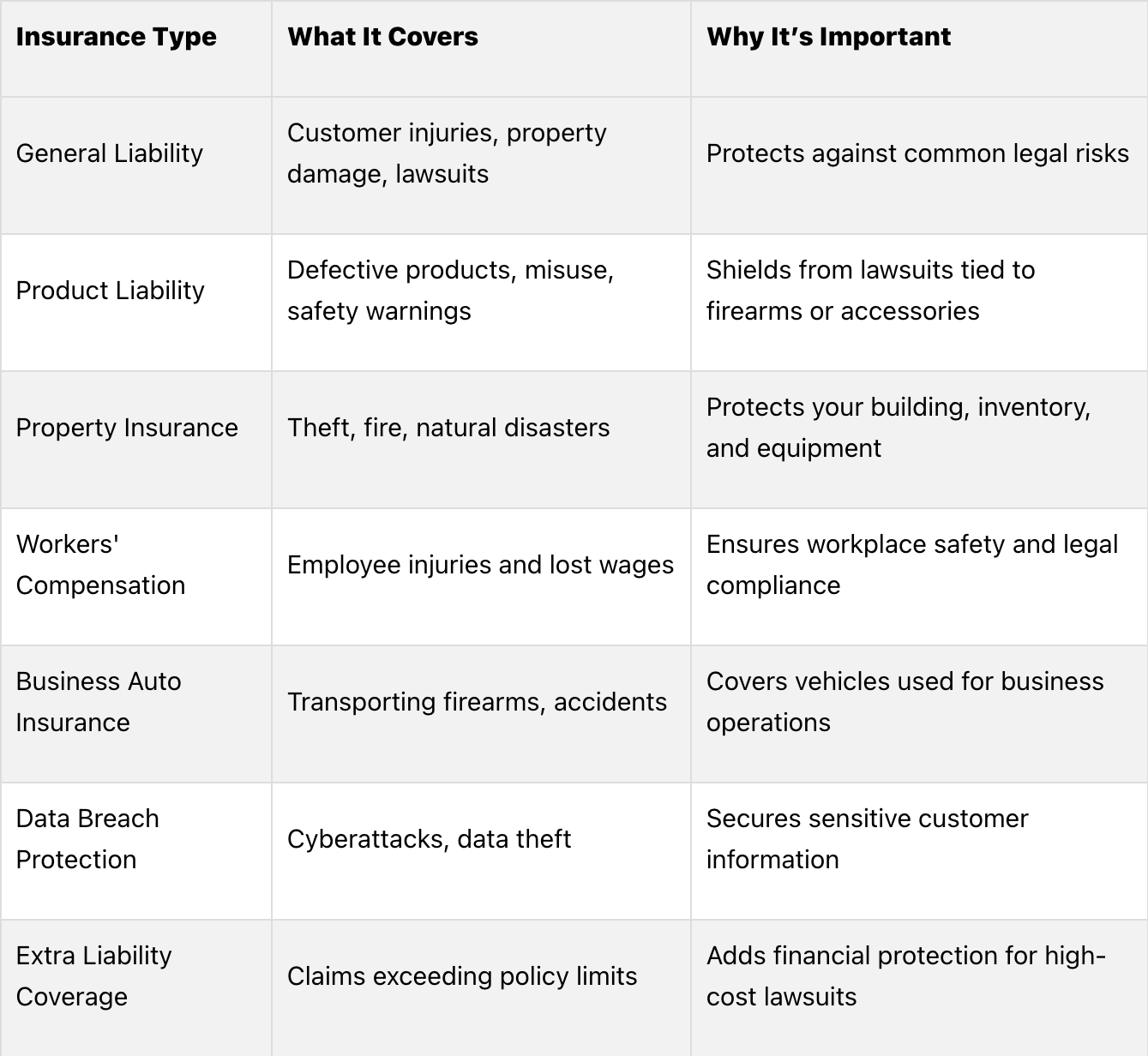

Running a gun shop comes with unique risks, from thefts to lawsuits. The right insurance can protect your business, employees, and customers. Here are the 7 essential insurance types every gun shop owner needs:

These insurance types help you stay compliant, manage risks, and ensure the long-term success of your business. Keep reading to learn how to choose the right coverage for your gun shop.

Every year, around 380,000 firearms are stolen in the United States, making security a top priority for gun shop owners[3]. Below, we break down the key risks that firearm retailers face and why having the right protections in place is essential.

The numbers speak for themselves: in 2022 alone, over 17,000 firearms were reported lost or stolen from federally licensed dealers[8]. Gun shops in states without dealer licensing face even greater challenges:

"Most FFL burglaries today are also committed by more than one individual, and stolen vehicles are frequently used to crash through a vulnerable access point to affect a smash-and-grab crime. Therefore, your 'impression of control' - what criminals will perceive to be obstacles to their success - will go a long way towards preventing a burglary."[6]

Firearm retailers face several liability risks that could lead to costly legal challenges:

Gun shops handle a wealth of sensitive customer information, from background checks to concealed carry permit applications. This data, along with point-of-sale records and electronic range waivers, must be carefully protected. In 2023, there were 7,275 violations tied to the misuse of a law enforcement database, highlighting just how vulnerable this information can be[9].

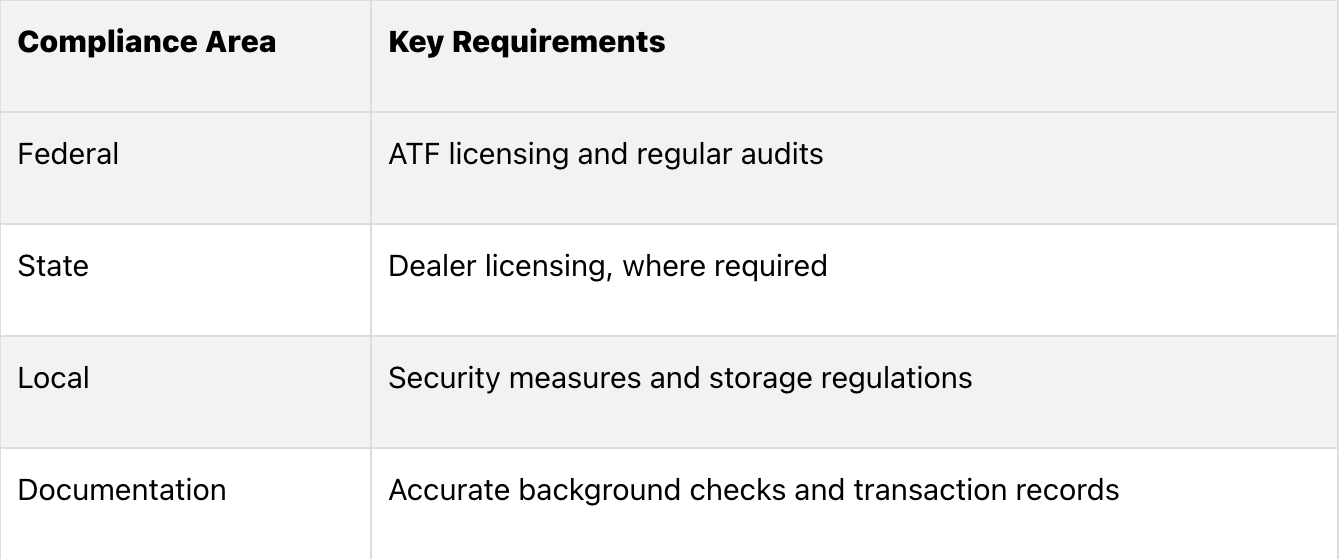

Operating within the firearms industry means adhering to a maze of regulations at every level:

Well-trained employees are a critical line of defense. They ensure safe firearm handling, enforce security protocols, and are often the first to spot potential threats[5].

"Bad guys start forming their opinions as they are driving around casing the joint. They're looking for opportunities to exploit or leverage a weakness."[7]

From physical security to compliance and liability, the risks gun shop owners face are varied and complex. These challenges make it clear why specialized insurance coverage is a must to safeguard these businesses and ensure their long-term success.

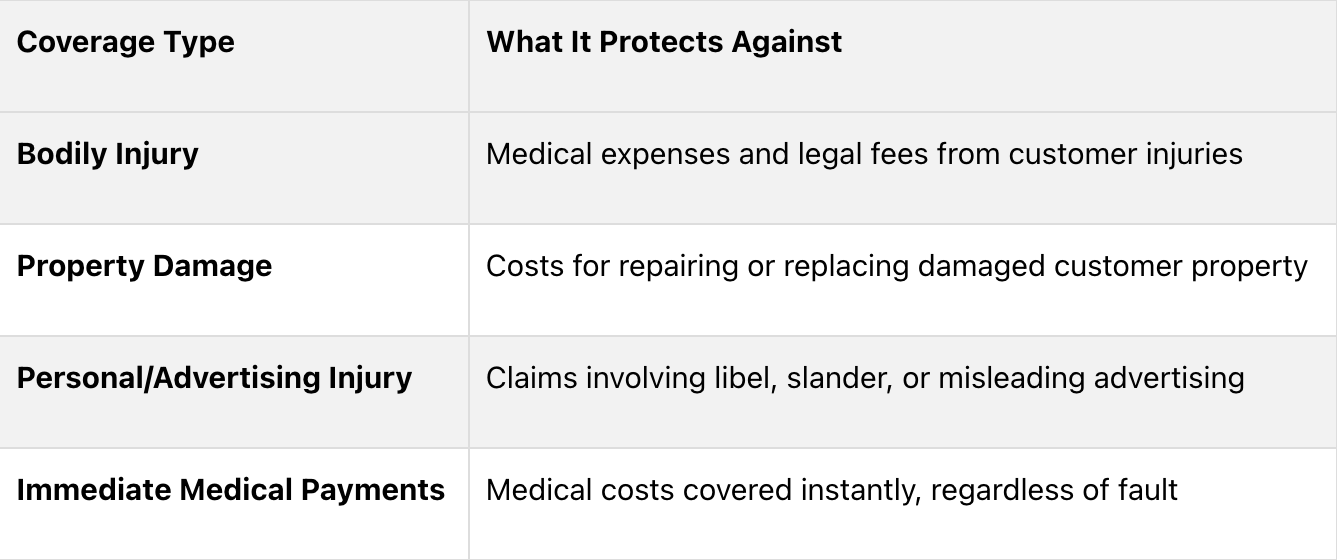

General liability insurance is a must-have for gun shop owners, offering protection against third-party claims for injuries, property damage, and even advertising-related issues. Considering there are over 51,000 gun stores across the U.S. [10], this type of coverage plays a critical role in safeguarding firearms retailers.

Here’s what a typical Commercial General Liability (CGL) policy covers:

This extensive coverage ensures gun shop owners can operate within the industry's strict regulatory framework.

Adhering to state and federal laws isn’t just a legal requirement - it’s essential for keeping your business afloat. Non-compliance can lead to hefty fines, lawsuits, or even losing your business license. To issue coverage, many insurance providers demand proof that your shop meets these legal standards. This added layer of scrutiny highlights the importance of having a strong insurance policy to manage the risks unique to the firearms industry.

Gun shops face some very specific risks that make tailored insurance coverage a necessity. Recent legal cases illustrate these challenges:

To address these kinds of risks, your CGL policy should include:

Taking steps like improving security measures and investing in staff training can also help reduce the likelihood of claims and may even lead to lower insurance premiums [5].

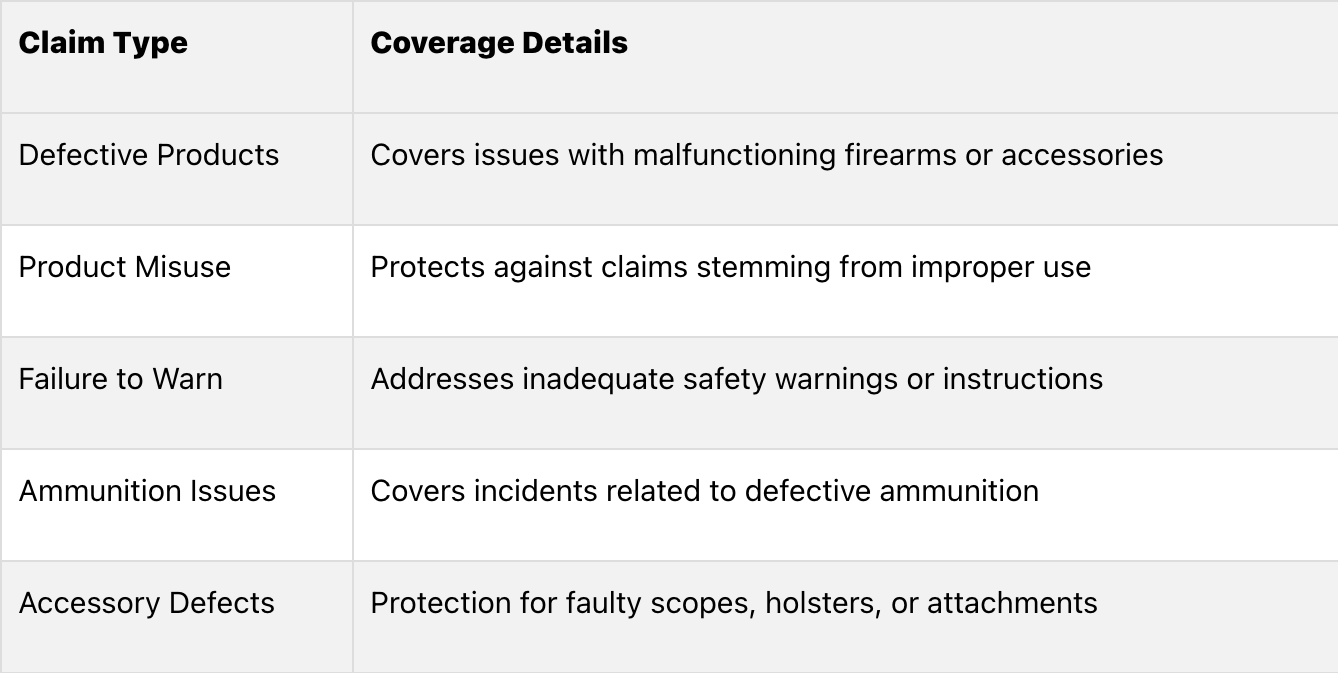

Product liability insurance is a critical safeguard for gun shop owners, offering protection against claims tied to defective products and related damages.

Here’s what it typically covers:

This coverage goes beyond standard liability insurance, addressing the distinct risks that firearms retailers face.

The Protection of Lawful Commerce in Arms Act (PLCAA) offers legal immunity to manufacturers and dealers in 34 states, shielding them from liability when their products are misused [12]. However, the legal landscape is shifting. For example, California has introduced legislation that would allow shooting victims to sue firearm manufacturers and sellers, signaling increased liability risks [1].

The importance of product liability insurance is underscored by cases like the $24 million awarded to a family after their son was killed by a defective firearm. The manufacturer, lacking adequate insurance, was forced into bankruptcy [14].

To minimize such risks, firearms retailers should:

With firearms-related incidents resulting in 48,830 deaths annually in the U.S. [12], having robust product liability protection is not just a precaution - it's a necessity for navigating an increasingly complex regulatory and safety environment.

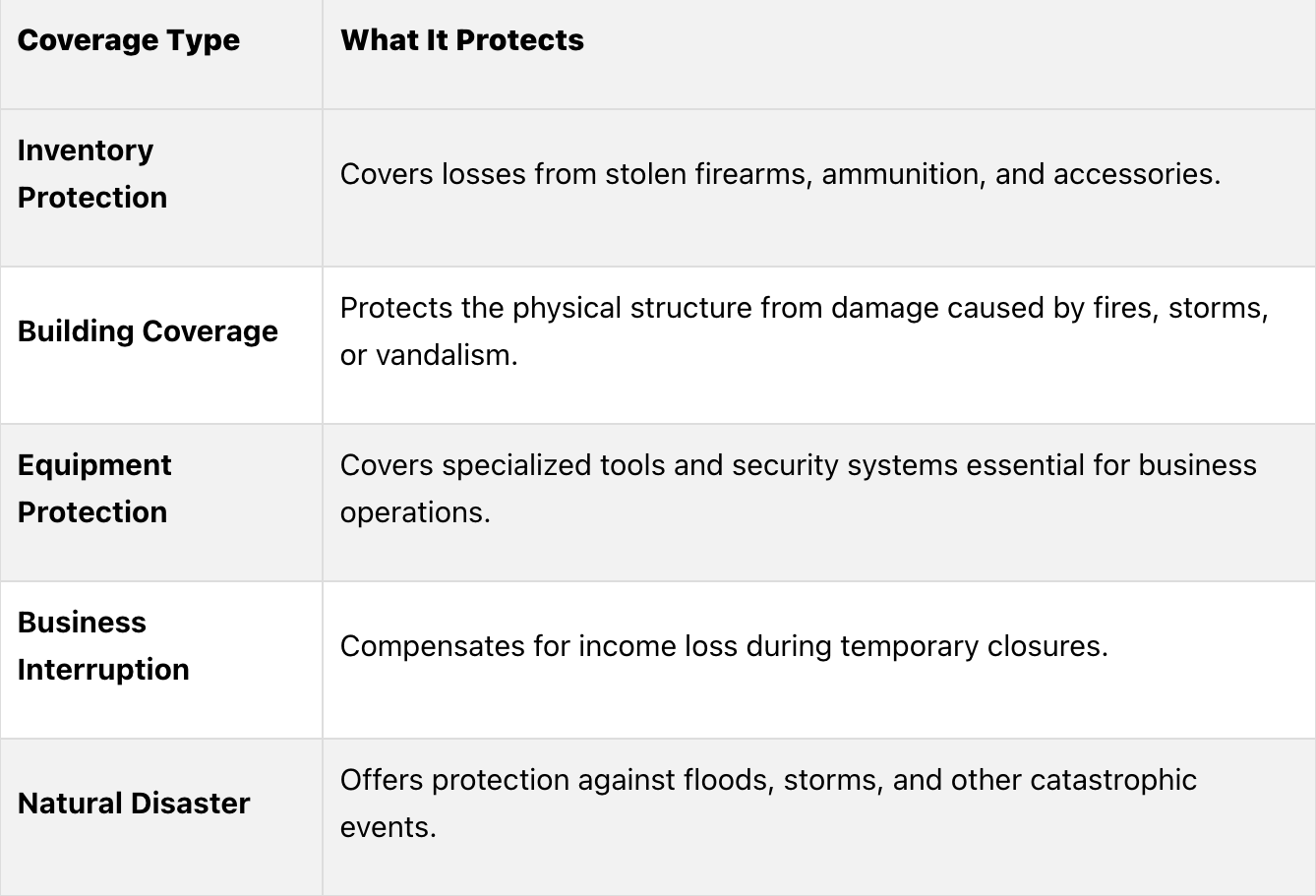

Property insurance is a critical safety net for gun shop owners, shielding them from risks like theft and natural disasters. With law enforcement reporting that over 200,000 firearms are stolen from licensed dealers every year [15], having strong insurance coverage is not just a precaution - it's essential for keeping the business running smoothly.

These coverage types are the foundation of a solid insurance plan, ensuring your assets are safeguarded while allowing you to focus on risk management tailored to your business.

In a country where around 380,000 firearms are stolen annually [3], firearms businesses face unique risks that demand both comprehensive insurance and effective security measures. To minimize these hazards, consider the following strategies:

These steps not only reduce the likelihood of theft but also ensure smoother claims processing if a loss occurs.

Insurance requirements for firearms businesses can vary significantly depending on your location. For instance, San Francisco mandates proof of adequate insurance before issuing firearms sales licenses [18]. On the federal level, dealers must certify that secure storage devices are available at every point of sale [17].

In 2022 alone, the property and casualty insurance sector wrote $729 billion in premiums [16]. This highlights the necessity of robust insurance coverage, particularly for businesses handling high-value and security-sensitive inventory. When combined with liability and product insurance, property coverage forms a comprehensive strategy to protect gun shop owners from the unique challenges of their industry.

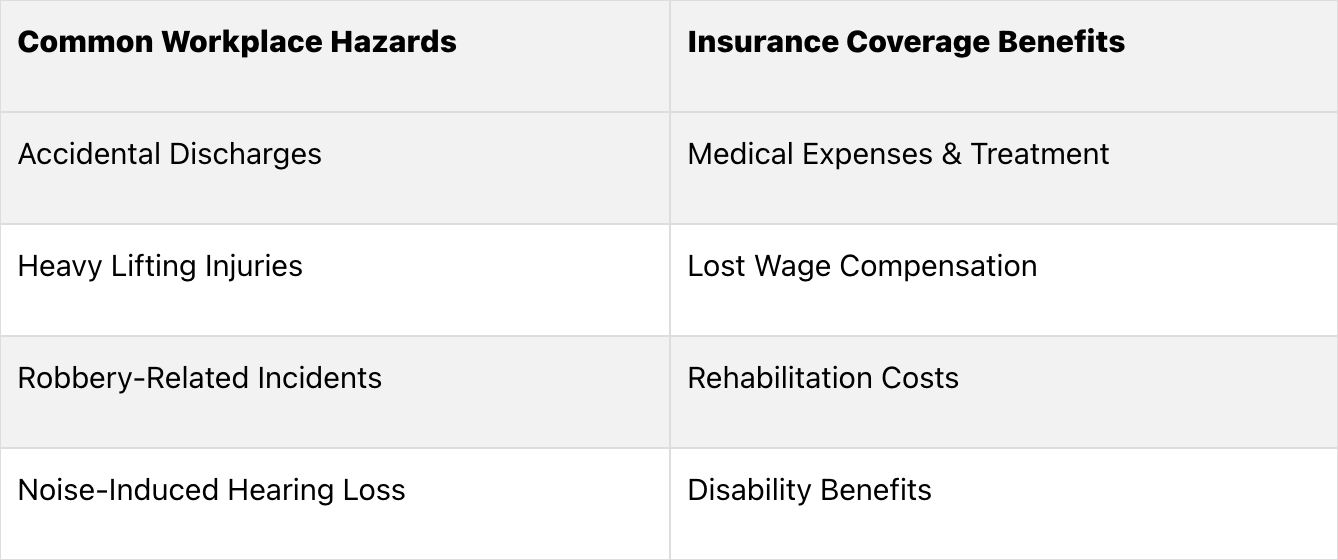

Just like property and liability insurance shield your business from common risks, workers' compensation is essential for safeguarding both your employees and your operations.

Workers' compensation insurance is designed to protect employees from workplace hazards, which are particularly relevant in the firearms industry. Risks such as accidental discharges, injuries from heavy lifting, and robbery-related incidents are all part of the job [19]. This type of coverage ensures that if an employee is injured on the job, they’ll have access to medical care and wage replacement.

Given these risks, implementing strong safety protocols is non-negotiable.

The firearms industry has seen its share of workplace accidents. For instance, in 2021, a gun shop owner in Berkeley County faced involuntary manslaughter charges after mistaking a GLOCK 17 for a BB gun [20]. In another case, an employee in Pinellas County accidentally discharged a .45-caliber handgun, injuring someone in a neighboring business [20].

To reduce these risks, consider the following steps:

These measures not only protect employees but also reduce the likelihood of accidents that could harm your business reputation.

Workers' compensation isn’t just about covering injuries - it’s also about staying compliant with the law. Failing to meet workers' comp requirements can lead to severe consequences, including hefty fines and even the suspension of your business license [21]. Many states have specific rules for firearms businesses, especially around how employees transport and handle weapons [22]. For example, Louisiana’s §292.1 outlines how firearms must be stored and transported in employees’ private vehicles on workplace premises [24].

Here’s how to stay compliant and reduce risks:

For gun shop owners, having business auto coverage is crucial when transporting firearms, ammunition, or other inventory [25]. This type of insurance is designed to protect vehicles used for business purposes - whether they're company-owned, leased, or even employee-owned. A Business Auto Policy (BAP) offers broader protection than personal auto insurance and is especially important for activities like:

These examples underscore why specialized auto policies are essential for safeguarding business assets and ensuring compliance during day-to-day operations.

When it comes to transporting firearms, compliance with both state and federal regulations is non-negotiable. Federal rules, for instance, mandate that firearms be locked and unloaded during transit, directly shaping how vehicles must be operated [26]. Gun shop owners also need to carry the proper permits and documentation at all times. As David Grimes aptly puts it:

"Knowledge is Safety. The more you know about what you're allowed to do and not allowed to do, the better chance you'll have to stay clear of trouble." [26]

This advice highlights the importance of understanding and adhering to the complex regulatory framework tied to firearms transportation.

Transporting sensitive and regulated inventory like firearms comes with unique risks. To minimize these risks, careful planning is a must. Routes should be mapped out in advance, and drivers need to be familiar with state-specific laws, particularly those related to concealed carry permits. Crossing state lines? Make sure all required permits and documentation are in order [26].

In addition to safeguarding physical assets and addressing liability concerns, gun shop owners must also consider the growing threat of cyber risks. With customer records increasingly stored digitally, data breach protection has become a must-have. This type of insurance helps cover both direct losses and liability-related expenses.

First-party coverage focuses on direct financial losses, including breach response costs, data restoration, business interruptions, cyber extortion, and funds transfer fraud. Meanwhile, third-party coverage addresses issues like network security liability, regulatory proceedings, PCI DSS compliance, legal defense fees, and settlement costs. Notably, third-party claims accounted for a significant 62.1% of the cyber insurance market in 2023 [27]. These policies are crucial, especially given the legal requirements surrounding customer data protection.

For instance, all U.S. states and territories mandate that businesses notify affected parties following a breach of personally identifiable information [29]. Data breach insurance helps businesses navigate these regulations and absorb the associated costs, reinforcing the need for robust cyber insurance.

"Cyber insurance is a rapidly evolving field and there is no one 'standard' policy. It's very important to know what you're buying. A good insurance broker will be able to tell you what is covered and what is excluded and can help design a policy that best meets your requirements. Insurance exists to help you transfer the risks that you cannot effectively mitigate yourself. However, insurance carriers will only cover the risks that you pay them to cover, so it's important to know what is and is not covered by your cyber policy." – Ken Mendelson, Managing Director, Stroz Friedberg [28]

Gun retailers are particularly attractive targets for cybercriminals due to the sensitive nature of the data they handle. A striking example is the August 2020 breach of the Utah Gun Exchange, where over 240,000 customer records were exposed on a hacking forum [31]. Cyber-attacks hit 43% of small businesses, with average breach costs reaching $4.88 million. Alarmingly, 60% of affected small businesses shut down within six months [27][30].

To reduce vulnerabilities, gun shop owners should combine cyber insurance with proactive security measures, such as:

The shift toward stand-alone cyber insurance policies is notable, with these now making up 68% of the market [27]. These policies offer more comprehensive protection than add-on options, which is critical as privacy-related class action lawsuits have tripled in value in recent years [27]. For firearm retailers, investing in adequate cyber coverage is not just about compliance - it's about ensuring the long-term survival of their business.

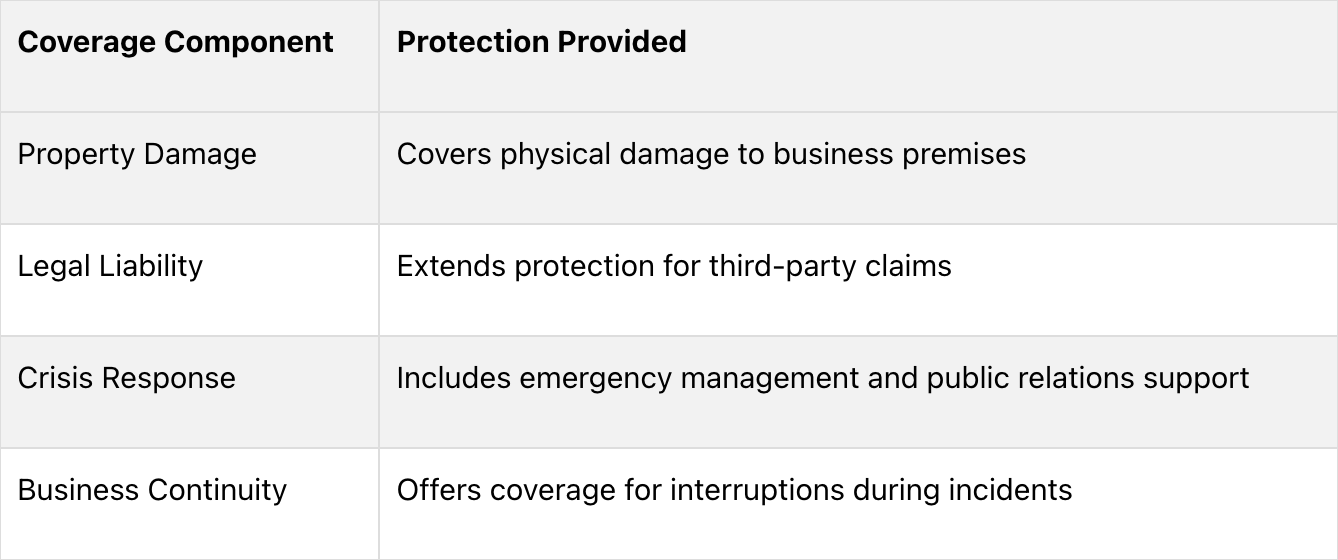

Extra liability coverage, often structured as a commercial umbrella policy, provides a safety net when standard policy limits are exceeded. Recent events have highlighted the need for this additional protection, especially as state regulations continue to evolve. This type of coverage helps close gaps left by standard policies, ensuring businesses are better prepared for unexpected situations.

Here’s what extra liability coverage can address:

Extra liability coverage is particularly relevant in meeting state-specific mandates that standard policies may not fully address. For instance, California requires $100,000 per occurrence for firearms-related businesses, emphasizing the need for tailored coverage. These regulations aim to hold manufacturers, distributors, and sellers accountable for higher risks associated with the industry.

"This bill is a significant step toward holding irresponsible, reckless, and negligent gun manufacturers, distributors, and sellers accountable." - Assemblymember Chris Ward [12]

By addressing uncovered risks, extra liability coverage aligns with these requirements and provides a critical tool for firearms businesses to stay compliant and protected.

Active shooter insurance, a specialized form of extra liability coverage, tackles risks unique to the firearms industry. It offers targeted provisions to manage potential incidents effectively:

FBI data reveals that from 2000 to 2023, there were 504 active shooter incidents in the U.S., resulting in 1,327 deaths and 2,314 injuries [11]. To mitigate these risks, gun shop owners should implement robust security measures like surveillance systems, intrusion detection, and emergency response protocols [32].

Although the Protection of Lawful Commerce in Arms Act (PLCAA) generally shields gun manufacturers and dealers from liability when their products are used in crimes, there are exceptions that could leave businesses vulnerable to significant claims [12]. This makes extra liability coverage an essential layer of protection against these unique hazards.

Important note: Since most insurers don’t offer standalone gun liability coverage [11], working with insurance professionals who understand the firearms industry is crucial to securing the right protection.

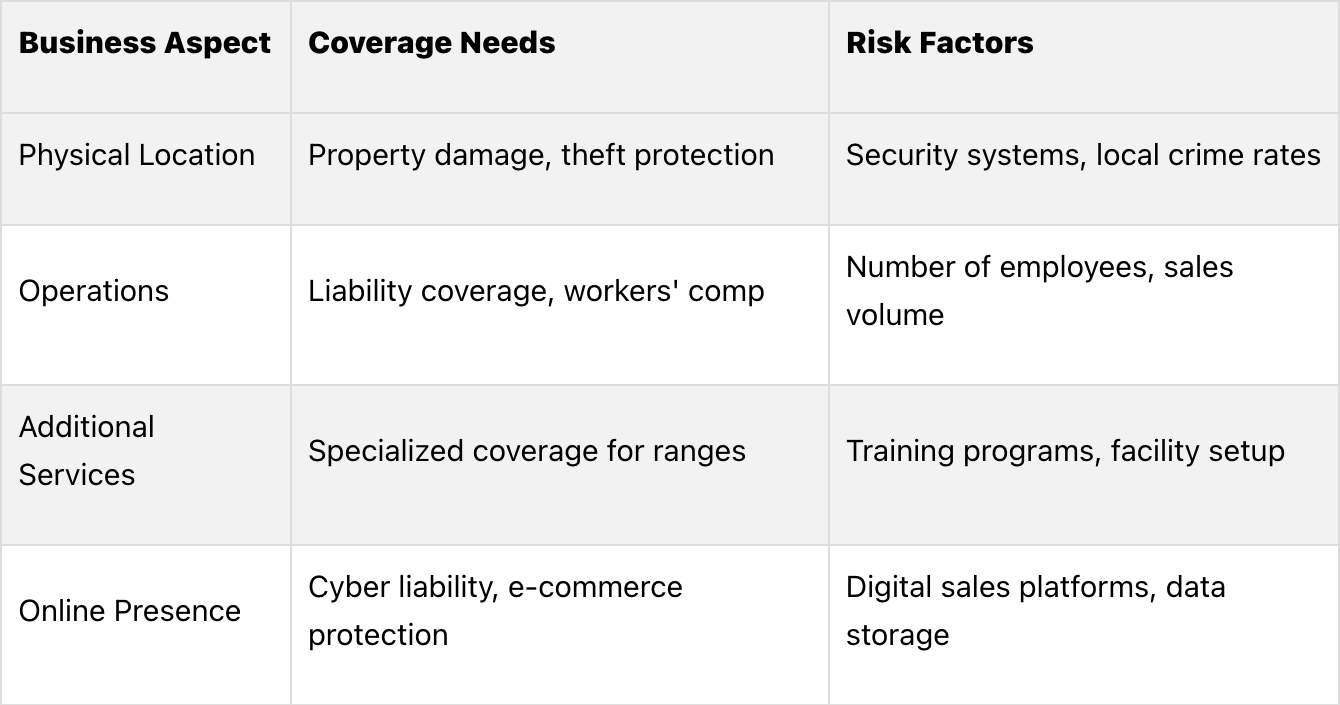

Choosing the right insurance means addressing the specific risks your shop faces. With over 52,000 licensed dealers in the U.S. alone, each business encounters its own challenges [4]. This highlights the importance of having coverage tailored to your needs.

A Business Owner's Policy (BOP) is a great starting point for gun shop insurance. It combines essential property and liability coverage. On average, a BOP costs $1,687 annually, or about $141 per month [34]. Keep in mind, actual costs will depend on your shop's unique risk factors and coverage requirements.

When comparing insurance policies, focus on these critical areas of your business:

Working with insurers who specialize in your industry is key. As Jack Napier puts it:

"If a customer is injured in your store, it could put you in bankruptcy, even if it's just a simple slip and fall" [35].

Between 2017 and 2023, law enforcement recovered 1.6 million firearms sold by licensed dealers [18]. This underscores the importance of having coverage that addresses both general and firearms-specific risks.

Customer endorsements can also highlight the value of working with experienced brokers. For example:

"A first class Insurance Broker representing the insured not the insurance company. They are the very best in the business!" - Fritz S. [2][33]

Gun shop owners must ensure their policies meet state-specific requirements. Some essential coverages include:

In 2023, nearly 15,000 firearms were reported lost or stolen from federal firearms licensees [18]. This highlights the need for theft coverage that not only protects your inventory but also complies with local regulations.

Bundling insurance policies can help save money while offering comprehensive protection. A Business Owner's Policy (BOP) typically includes property, liability, and business interruption coverage, with optional add-ons available. Gun shops often face higher insurance premiums compared to other businesses [3]. That’s why it’s crucial to partner with providers who understand the unique risks of the firearms industry and can offer competitive rates on bundled packages.

Running a gun shop comes with unique risks, making the right insurance coverage critical. In 2021 alone, there were 48,830 firearm-related deaths [11], underscoring the importance of having solid insurance protection - not just as a business decision but as a safeguard for long-term success.

Specialized insurance providers understand the specific challenges faced by firearm businesses. They offer tailored solutions to help mitigate both general and industry-specific risks. A well-designed insurance plan does more than protect - it reflects your commitment to operating responsibly. The right insurance partner can:

The value of expert guidance in navigating these complexities is evident in customer feedback:

"Their service has been outstanding. I would strongly recommend them to any gun dealer in need of insurance for their business." – Charles K. [36]

Proper insurance coverage doesn't just shield your business - it contributes to broader safety and accountability within the industry. As risks shift and regulations evolve, regularly reviewing and updating your policy ensures it stays effective and aligned with your needs.

Gun shop owners deal with a unique set of challenges that make tailored insurance coverage a must-have. One of the biggest concerns? Legal liabilities. Lawsuits can arise from injuries caused by firearms or ammunition sold at your store, putting your business at significant financial risk. On top of that, strict federal and state regulations demand compliance, and falling short could mean steep fines or legal trouble.

Theft and burglary are also constant threats. Firearms and ammunition are high-value items, making gun shops prime targets for criminals. Then there’s employee safety to think about. Workers handling heavy inventory or firearms face the risk of injury, making workers' compensation coverage essential. And let’s not forget the potential for accidental discharges inside the store - an incident like that could lead to severe injuries and costly liability claims.

The right insurance coverage doesn’t just protect against these risks - it helps your business stay prepared for whatever comes its way.

To make sure their insurance coverage aligns with state and federal laws, gun shop owners need to start by understanding the legal obligations tied to their business. A key step is obtaining a Federal Firearms License (FFL), mandated by the Bureau of Alcohol, Tobacco, Firearms and Explosives (ATF), which ensures adherence to federal rules governing firearm sales and distribution. Beyond federal regulations, it's equally important to dive into state-specific laws, as these can differ significantly and often come with additional requirements.

Partnering with an insurance provider that specializes in firearm-related businesses can be a smart move. These providers are well-versed in the unique risks gun shops face and can help craft coverage that meets both state and federal legal standards. By aligning their insurance policies with these regulations, gun shop owners not only safeguard their business but also ensure full compliance with the law.

To keep your gun shop safe from cyber threats and data breaches, start with the basics: enforce strong password policies and educate your team on cybersecurity best practices. Protect sensitive customer and business information by securing both physical and digital access. Tools like firewalls, encryption, and multi-factor authentication are essential here. Also, make it a habit to update your software and systems regularly to fix vulnerabilities, and schedule frequent security audits to catch potential risks early.

It's equally important to have a clear response plan in place for data breaches. Your team should be prepared to act quickly and effectively if an incident happens. Staying up to date with cybersecurity trends and using resources like industry guidelines can further bolster your defenses. These measures not only protect your business but also help preserve the trust of your customers in a highly regulated space.

If you're looking for reliable gun business workers comp solutions that actually fit your operation, now’s the time to take the next step. Don’t wait until there’s a problem—get ahead of it with the right coverage and support. We’re here to help firearm businesses across New Jersey stay protected, stay legal, and keep things running smoothly. Reach out today to see how we can help you get set for 2025.

Call Now: 800-526-2199. Or submit your inquiry below. We look forward to having the opportunity to work with you!