What insurance do firearms dealers need in California?

California requires $1 million general liability insurance, one year of video storage, and employee training by 2026.

Does New York require insurance for gun dealers?

No set minimum, but liability exposure is high. Dealers must keep two years of video, train employees, and post safety warnings.

What are the insurance rules for firearms dealers in Texas?

Texas has no mandatory coverage, but liability and property insurance are strongly recommended.

What insurance coverage should all firearms dealers carry?

General liability, property insurance, workers’ comp, and product liability coverage.

How do video surveillance rules affect firearms dealers?

Strict video retention (1–2 years) boosts compliance and can help with insurance approvals and risk assessments.

What compliance steps reduce ATF and liability risks?

Accurate A&D records, regular audits, employee background checks, and strong security systems.

•••

Running a firearms dealership? Here's what you need to know about state-specific insurance requirements:

Staying compliant involves proper record-keeping, employee background checks, and robust security measures. Non-compliance risks losing your license or facing hefty fines.

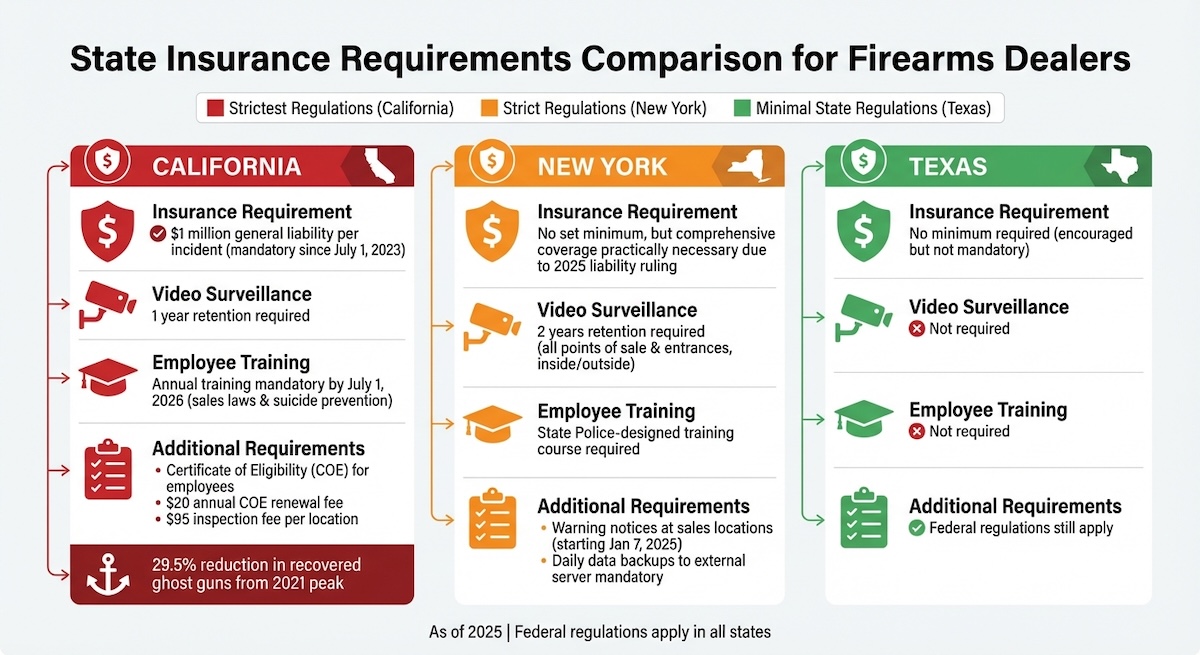

California enforces some of the strictest insurance and operational requirements for firearms dealers in the country. Since July 1, 2023, every licensed dealer must maintain general liability insurance with a minimum coverage of $1 million per incident - a prerequisite for obtaining and renewing a license [1]. Beyond insurance, the state requires dealers to implement digital video surveillance systems capable of recording and storing footage for at least one year [1]. This ensures a robust monitoring system for all transactions and activities.

By July 1, 2026, California will also mandate annual training for employees handling firearms, focusing on sales laws and suicide prevention [4]. Employees must already hold a valid Certificate of Eligibility (COE) issued by the Department of Justice, a rule in place since 2018. Dealers are responsible for paying an annual COE renewal fee of $20.00, along with a $95.00 inspection fee per location [7].

California’s rigorous oversight appears to be yielding results. For example, enhanced tracking measures contributed to a 29.5% reduction in recovered unserialized "ghost guns" from their peak in 2021 [8].

New York takes a different but equally stringent approach to regulating firearms dealers. While the state doesn't specify a minimum liability insurance amount like California, a 2025 federal appeals court ruling has heightened the stakes. This decision allows gun manufacturers and dealers to be held liable for deadly shootings involving their products, making comprehensive coverage - including general liability, property, and product liability insurance - a practical necessity [5].

New York’s video surveillance rules are even more demanding than California’s. Dealers must record activity at all points of sale and entrances, both inside and outside, and retain the footage for two years [6]. Additionally, all employees must complete a training course designed by the State Police [6]. Starting January 7, 2025, dealers will also be required to display warning notices at sales locations, educating customers about firearm risks and proper storage [5]. For those using electronic record systems, daily data backups to an external server or online platform are mandatory [6].

These measures reflect New York’s emphasis on accountability and public safety, setting a high bar for compliance.

Texas adopts a more relaxed regulatory stance compared to California and New York. The state doesn't enforce minimum liability insurance requirements, but Federal Firearms License (FFL) holders are strongly encouraged to carry property and liability insurance to mitigate potential business risks [9].

Unlike the other states, Texas doesn’t mandate specific training programs or video surveillance systems for dealers. This gives dealers more autonomy in their operations. However, federal regulations still apply, and maintaining adequate insurance remains a smart business practice to address potential liabilities.

While Texas offers fewer state-level restrictions, the operational risks faced by firearms dealers remain consistent across the board, underscoring the importance of voluntary compliance with best practices.

State laws may set minimum insurance requirements, but having the right coverage can shield your business from the risks firearms dealers face daily. Each type of insurance serves a unique purpose, offering protection tailored to your operations.

This type of insurance safeguards your employees from workplace hazards like lead exposure, hearing damage, accidental discharges, or injuries caused by heavy lifting. If your firearms business employs staff, workers' compensation insurance isn't optional - it's required. Failing to comply could lead to license suspension or hefty fines.

Firearms business and property insurance covers your inventory, equipment, and premises against threats like fires, natural disasters, vandalism, and theft. Many policies also include "Inland Transit" coverage, which protects inventory while it's being transported, and "Business Income Protection", which helps recover lost revenue during temporary closures. Starting in 2025, insurers increasingly demand proof of advanced security measures - such as biometric safes or reinforced storefronts - before approving property and liability coverage [3].

This insurance is your safety net for third-party claims, whether it’s bodily injury, property damage, or advertising-related issues like libel or copyright infringement. It also helps cover legal fees and settlements. In many states, comprehensive liability coverage is mandatory. For example, California requires firearms dealers to maintain at least $1 million in coverage per incident [1]. Other states have similar mandates for commercial general liability, product liability, and broad form vendors' insurance [10].

One critical feature to look for is product liability coverage. Even if you’re not the manufacturer, you could still be held responsible for claims involving defective firearms, ammunition, or accessories. Retailers often face strict liability alongside manufacturers for product malfunctions, making this coverage essential for protecting your business in such a high-stakes industry.

Staying on top of compliance means keeping detailed records, conducting thorough employee screenings, and implementing strong risk management strategies. These efforts not only fulfill state requirements but also align with the specialized insurance services offered by Joseph Chiarello & Co., Inc.

The urgency of compliance has grown, especially with ATF inspections leading to 195 license revocations in fiscal year 2024 - a staggering 122% jump from FY 2022 [12].

Every firearm transaction must be recorded in your A&D Bound Book by the end of the next business day. Keep ATF Form 4473 records for at least 20 years for approved transfers and 5 years for denied ones [12]. In FY 2024, only 54% of inspected FFLs were found free of violations, with nearly 100,000 individual violations reported nationwide [12].

To stay compliant, conduct quarterly inventory checks and review Form 4473 regularly to catch and correct errors before they escalate [12]. Switching to digital FFL software can also reduce clerical mistakes compared to paper-based logs [12].

In California, additional rules apply. Dealers must maintain video surveillance records for at least one year and ensure annual system certifications with maintenance logs [1]. Proof of insurance is also critical - California requires at least $1 million in general liability coverage per incident [1].

Keeping accurate records and conducting regular reviews is key to avoiding violations and ensuring compliance.

Screening employees thoroughly not only protects your business but also shows insurers and regulators that you’re taking compliance seriously. Keep all background check documents, including consent forms and results, for at least 5 years [11]. The cost of a background check in the firearms industry is $16.45 per applicant [11].

Verify applicant details using government-issued photo IDs and Social Security services to ensure consistency across all documentation [11]. In states where NICS can be used for employment screening, remember to use Purpose ID 57 during the process [11]. Starting July 1, 2026, California will require all licensees and employees handling firearm transfers to complete annual training on spotting illegal activities and identifying signs of self-harm [1].

Detailed background checks combined with proper documentation help safeguard your business and maintain compliance.

Strong security measures can reduce risks while also lowering insurance premiums. Use hardened steel rods or cables (at least 1/8 inch thick) through trigger guards, or store inventory in locked, fireproof safes or vaults [1]. Secure ammunition in a way that requires staff assistance for access [1].

Post required warnings about child access, lead exposure, and suicide prevention clearly in your store [1]. Additionally, have a clear protocol for reporting firearm or ammunition loss or theft to local law enforcement within 48 hours of discovery [1]. These steps not only meet legal requirements but also demonstrate responsible practices that insurers value, potentially leading to reduced premiums.

Firearms dealerships face a patchwork of state requirements, making it essential to stay informed about your specific mandates. Understanding these regulations is key to keeping your license intact and avoiding penalties or even revocation.

Insurance plays a critical role in protecting your business from various risks, including emerging threats like cybersecurity breaches. Securing the right coverage does more than meet legal obligations - it provides a safety net for your operations and ensures legal support as state laws continue to evolve [2].

Strong record-keeping, consistent inventory audits, and effective security measures not only help with compliance but also make your business more appealing to insurers. These practices can simplify the underwriting process and potentially reduce your premiums [3].

With increasing industry standards [1], having comprehensive liability protection ensures your dealership stays compliant. Aligning your insurance policies with state regulations and proactive risk management helps reduce liability exposure while strengthening your business's ability to adapt and thrive.

For tailored advice on navigating state-specific rules and finding the right insurance coverage for your dealership, reach out to Joseph Chiarello & Co., Inc. for expert support.

If your state doesn’t mandate minimum insurance requirements, it’s a smart move to consider carrying comprehensive coverage to safeguard your firearms business. Some key insurance policies to look into include:

These policies help ensure you’re prepared for various risks and liabilities that could impact your business.

Video surveillance regulations, like California's mandate for round-the-clock digital video and audio recording systems, can lead to higher compliance costs for businesses. On the upside, these systems can improve security and demonstrate a lower risk profile to insurers. This added security could make insurance approvals smoother and might even help reduce premiums over time.

Maintaining detailed records of firearm transactions, inventory, and employee background checks is crucial for reducing ATF and liability risks. Staying compliant with both federal and state laws is equally important. Regular internal audits can help confirm that all regulations are being followed. These steps not only show responsibility but also help lower potential risks.

Don't wait until it's too late to make sure your gun shop is covered. At Joseph Chiarello & Co., Inc., we’re here to help you navigate the ins and outs of gun shop workers compensation insurance to ensure you're prepared for any noise-related risks, including hearing damage. Reach out to us today to review your current policy or get a customized quote. Protect your team and your business with the right coverage—because their safety is worth it.

Call Now: 800-526-2199. Or submit your inquiry below. We look forward to having the opportunity to work with you!